State of Luxury Brands in 2026: When Consumption Rises but Luxury Stays Locked

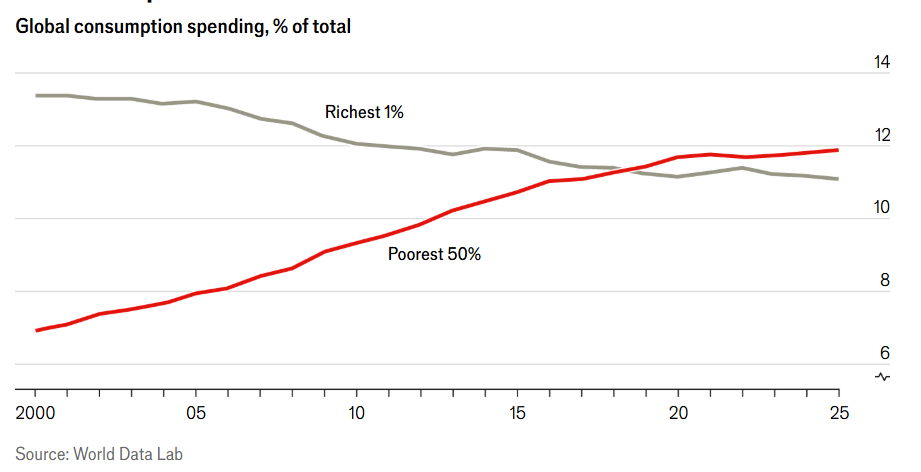

In 2026, the global economy is telling an unexpectedly optimistic story. Data cited by The Economist (World Data Lab) shows that since 2000, the spending gap between the world’s richest 10 percent and poorest 50 percent has more than halved.

Consumption in emerging markets such as China, India, and the Middle East has grown rapidly. The spending gap between the average American and the average Indian has narrowed significantly over the past 25 years. By one important measure, the world is becoming less unequal in terms of consumption.

Yet in 2026, luxury brands are encountering resistance as global consumption is broadening. Growth has slowed across key markets. Aspirational demand is under pressure. Consumers are hesitating in ways that would have seemed unlikely during the post-pandemic surge.

This creates a striking paradox: if more people around the world are earning and spending more, why is luxury not expanding proportionately into this newly strengthened middle tier?

Convergence does not automatically create luxury buyers

The narrowing of global consumption inequality reflects economic convergence between countries, particularly driven by growth in low- and middle-income economies. Millions of households in markets such as India now command higher purchasing power than they did two decades ago.

On paper, this expanding global middle should represent fertile ground for luxury brands seeking long-term growth.

However, rising consumption does not automatically translate into luxury participation. Luxury does not operate purely on income thresholds; it operates on perceived surplus and psychological comfort.

A household may be earning and spending more than before, yet still feel financially constrained by housing costs, education expenses, healthcare pressures, or job uncertainty.

In many economies, rising consumption has coincided with heightened financial anxiety rather than carefree confidence.

Luxury depends not only on disposable income but on a sense of security. When consumers feel stable and optimistic about the future, they indulge. When economic advancement feels fragile or hard-won, spending becomes more calculated. The global middle class may be larger, but it is also more cautious.

The price escalation strategy

Over the past decade, and particularly during the post-pandemic rebound, luxury brands aggressively escalated prices. Handbags, ready-to-wear, sneakers, and even entry-level accessories moved steadily upward. What was once considered “aspirational luxury” now sits closer to the price of bands historically associated with heritage exclusivity.

In his Adweek column, “The $1,000 Gucci T-Shirt Problem,” Mark Ritson argues that luxury brands may have mistaken temporary momentum for permanent pricing immunity.

During the boom, price increases were absorbed with little visible resistance. Demand appeared resilient, and brands interpreted this as structural inelasticity.

That interpretation is now being tested. Elasticity was obscured by extraordinary circumstances, including stimulus-driven spending, post-lockdown exuberance, and a surge in speculative consumption.

As those forces normalize, price sensitivity re-emerges. When entry-level products begin to feel disconnected from perceived value, consumers hesitate. The issue is not an absence of global growth but a mismatch between income progression and price acceleration.

When luxury moves faster than the middle

The core tension in 2026 lies in relative movement. While global consumption inequality between nations has narrowed, luxury pricing has outpaced that convergence.

Middle-income consumers in emerging markets are objectively stronger than they were 20 years ago, but the cost of entry into major European fashion houses has increased at a faster rate.

In effect, as the global middle class climbed upward, luxury simultaneously elevated its threshold.

Luxury brands often assume that as more consumers move into higher income brackets, the addressable luxury audience expands automatically. In reality, luxury penetration depends on the relationship between income growth and perceived value.

If pricing rises faster than income confidence, the gap remains intact. The ladder may have shortened globally, but luxury has extended its top rung.

This dynamic becomes especially visible among aspirational consumers. The ultra-high-net-worth segment remains relatively insulated, but the middle-tier luxury buyer is more discerning.

Digital transparency allows consumers to compare craftsmanship, materials, and markups with unprecedented clarity. The symbolic aura of the logo is no longer sufficient on its own to justify steep price hikes.

Spending power versus spending confidence

Another nuance within the convergence narrative is the distinction between spending and security. The data reflects how much people are consuming, not how secure they feel.

Asset ownership remains unevenly distributed, and wealth inequality in property and financial markets persists even as consumption gaps narrow. In many countries, political and technological uncertainties add to a broader sense of instability.

Luxury thrives on confidence. It depends on a consumer’s willingness to display, to signal, and to indulge publicly.

In an era marked by economic caution and cultural sensitivity toward overt displays of wealth, conspicuous consumption carries more friction. The rise of understated or “quiet” luxury reflects this shift in tone.

Consumers may still desire quality and craftsmanship, but they are less inclined to embrace overt extravagance without justification.

As a result, even in a world where consumption equality is improving, luxury brands are not automatically gaining entry into new segments. The global consumer base may be expanding, but the psychological conditions that fuel aspirational luxury are more complex.

The strategic implication for 2026

Luxury must now confront a more demanding environment in which pricing power is not assumed but scrutinized. If brands wish to penetrate newly empowered middle markets, they must recalibrate their value of architecture. Exclusivity must be credible, and access must feel intentional rather than opportunistic.

The global economy may be converging, but luxury is not automatically included in that convergence. More consumers exist with the capacity to spend, yet fewer feel naturally invited into the luxury equation at current price levels.

That tension defines the industry’s new reality: growth is broadening globally, but luxury access remains constrained by strategy rather than by pure economics.

Cut to the chase

The challenge for luxury brands in 2026 is not a lack of global growth. It is a strategic misalignment between macroeconomic convergence and brand-level pricing strategy.